What is a Mortgage? Complete Step-by-Step Guide (2023)

Buying a home is one of the most important financial decisions that most peoples make in their life. For most people, a home is not only a place to live but also an investment. Unfortunately, purchasing a home requires a significant amount of money, which most individuals do not have easily accessible. This is where a mortgage may help.

In this article, we’ll look at what a mortgage is, how it works, the different types of mortgages accessible in the United States and other countries as well, and some real-world instances of how mortgages are utilized.

What is a Mortgage?

A mortgage is a loan that you take out to buy a property. The property you purchase acts as collateral for the loan, which means that if you fail to repay the loan, the lender can take and sell the property to recover the money. A mortgage is often a long-term loan that needs regular payments (usually monthly) until the debt is paid off.

Why is it called a Mortgage?

The word “mortgage” comes from the Old French word “mort” which means “dead” and “gage” which means “pledge”. Essentially, a mortgage is a pledge that becomes “dead” or “null” once the loan is fully repaid.

How do Mortgages Work?

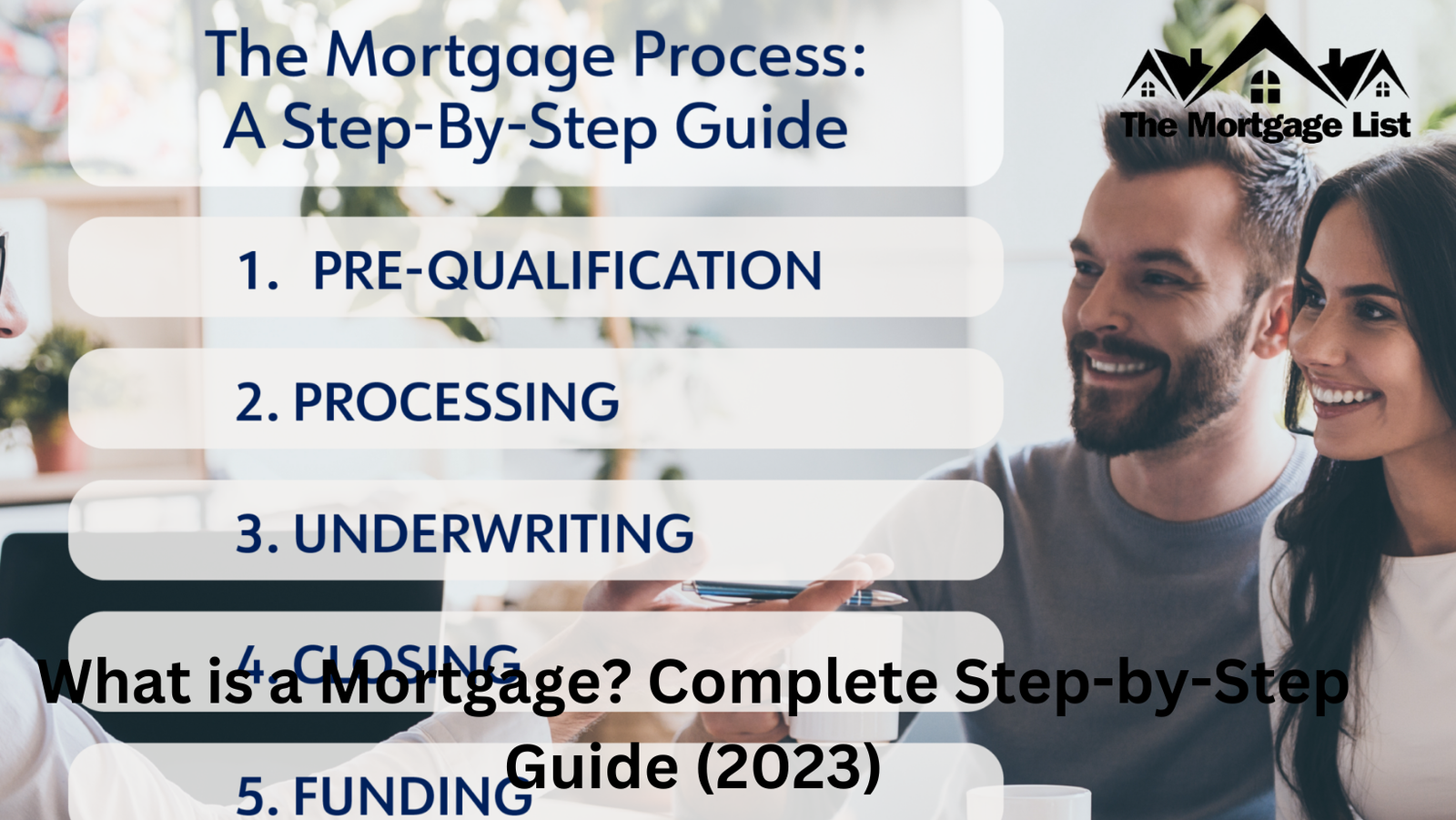

The mortgage process typically starts with prequalification and preapproval. Pre-qualification is an informal process that estimates how much you can borrow based on your income, assets, and debts. Pre-approval is a more formal process in which the lender verifies your financial details and creditworthiness and approves you for a specified loan amount.

You can begin house-looking once you have received pre-approval. When you identify a property that you wish to acquire, you will make an offer to the seller, and if they accept, you will sign a purchase agreement. The purchase agreement will include a clause stating that the acquisition is conditional on you obtaining financing. You’ll apply for a mortgage at this stage, and the lender will look over your information, including your credit score, income, debt-to-income ratio, and employment history.

If the lender approves your mortgage application, you will receive a loan estimate outlining the loan’s conditions and expenses. The loan estimate will include the interest rate, loan amount, and monthly payments predicted. You’ll also receive a Closing Disclosure, which outlines the loan’s final terms and expenses. Before the loan may be funded, you must study and sign the Closing Disclosure.

Types of Mortgages

There are several types of mortgages available in the US, each with its own features and benefits. Here are some of the most common types of mortgage loans:

1. Fixed-Rate Mortgages

A fixed-rate mortgage is one with an interest rate that remains constant throughout the loan’s term. This implies that your monthly payments will remain the same, making planning for your mortgage payments easier. Fixed-rate mortgages are popular because they provide predictability and stability.

2. Adjustable-Rate Mortgage (ARM)

An adjustable-rate mortgage (ARM) is a mortgage with an interest rate that can change over time. ARM interest rates are typically lower than fixed-rate mortgage interest rates, at least initially. Nevertheless, after a specific period of time (typically 5 to 10 years), the interest rate might adjust annually, causing your monthly payments to rise or fall.

3. Jumbo Mortgages

Jumbo mortgages are home loans that exceed the limits set by Fannie Mae and Freddie Mac. They are often used for high-end houses and can provide financing for residences with loan amounts that exceed the conforming loan limit.

Jumbo mortgages have higher interest rates and more strict qualification standards, such as higher credit scores and lower debt-to-income ratios. To find the best jumbo mortgage option for your circumstances, shop around and compare offers from multiple lenders. Jumbo mortgages are not available from all lenders, and those that do may have different requirements and qualifications.

4. Government-Insured Mortgages

Mortgages backed by the federal government are known as government-insured mortgages. These mortgages are intended to make homeownership more accessible to borrowers with low and moderate incomes. FHA loans, VA loans, and USDA loans are all examples of government-insured mortgages.

Who Provides Mortgage Loans?

Mortgage loans are typically provided by banks, credit unions, and other financial institutions. These lenders check applicant creditworthiness and ability to repay loans using indicators such as income, credit history, and debt-to-income ratio.

Aside from typical lenders, there are also specialized mortgage lenders who specialize in certain types of borrowers or properties. For example, some lenders specialize in providing mortgages for first-time homebuyers, those with poor credit, or those looking to finance investment properties.

Mortgage brokers are yet another alternative for consumers seeking a mortgage loan. Brokers operate as go-betweens for both lenders and borrowers, helping in matching borrowers with lenders that fit their individual needs and requirements.

Finally, some government agencies also offer mortgage loans or insurance programs to assist in making homeownership more affordable. For example, the Federal Housing Administration (FHA) provides mortgage insurance to borrowers who may not qualify for typical mortgages due to low credit scores or minimal down payments.

How to Find the Best Mortgage Rate

Finding the best mortgage rate is important when buying a home. Your mortgage’s interest rate can have a substantial impact on your monthly payments as well as the total amount you’ll pay throughout the life of the loan. Here are some tips to help you discover the best mortgage interest rate:

1. Check your credit score

Your credit score has a significant impact on the interest rate you’ll receive on your mortgage. Check your credit score before applying for a mortgage and resolve any inaccuracies or concerns that may be decreasing your score.

A higher credit score may enable you to qualify for cheaper interest rates and more favorable loan arrangements.

2. Shop around

Don’t accept the first mortgage offer you receive. To locate the best offer, shop around and compare rates from other lenders. Start with your bank or credit union, but don’t be hesitant to look into other lenders as well.

Internet mortgage comparison tools can also help you compare rates and costs from various providers.

3. Consider different loan terms

The loan term is the amount of time you have to repay the loan. A shorter loan period may result in a higher monthly payment, but you will pay less interest overall. A longer loan term, on the other hand, may result in a cheaper monthly payment, but you will pay more in interest over the life of the loan. While deciding on a loan term, keep your budget and financial goals in mind.

4. Decide on a fixed or adjustable rate

Mortgage rates are classified into two types: fixed and adjustable.

| Fixed Rate Mortgage | Adjustable Rate Mortgage |

| A fixed-rate mortgage has an interest rate that is fixed for the duration of the loan. | An adjustable-rate mortgage (ARM) has an interest rate that can alter based on market conditions on a regular basis. |

| Fixed-rate mortgages provide greater stability. | Adjustable-rate mortgage are riskier but may provide lower starting interest rates. |

5. Consider points and fees

Mortgage points are upfront costs that you pay to lower your interest rate. Each point costs 1% of the loan amount and reduces the interest rate by 0.25%. Think about whether paying points makes sense in your situation.

While evaluating mortgage offers, you should also consider other fees such as origination fees, application fees, and appraisal fees.

So, finding the best mortgage rate requires some research and shopping around. Check your credit score, compare rates from several lenders, think about different loan lengths and types, and consider points and costs. You may find a mortgage that meets your budget and financial goals with some effort and care.

Mortgage List

Here are some mortgage provider company reviews.

Mortgage: Residential vs Commercial

Mortgages can be used to finance both residential and commercial buildings, but there are some key differences between the two.

| Residential Mortgage | Commercial Mortgage |

| Residential mortgages are used to finance homes that are primarily occupied by individuals or families. These can include single-family homes, townhouses, and condominiums. | Commercial mortgages are used to finance commercial properties such as office buildings, warehouses, and retail spaces. |

| Household mortgages have lower interest rates and longer repayment durations than commercial mortgages because lenders regard them to be less risky investments. | Commercial mortgages often have higher interest rates and shorter repayment durations than residential mortgages because lenders view them as greater risk investments. |

How to Compare Mortgage?

Comparing mortgages can be overwhelming, but it’s essential to find the best deal. Here are some things to consider when comparing mortgages:

- Interest Rate: The interest rate is the cost of borrowing money and determines your monthly payment as well as the total amount you pay throughout the life of the loan.

- Loan Term: The loan term is the amount of time you have to repay the loan. Lower monthly payments will result from a longer loan term, but you will pay more interest throughout the life of the loan.

- Loan Type: Mortgages come in a variety of flavors, including fixed-rate, adjustable-rate, and government-backed loans. Each sort of loan has advantages and disadvantages, so it is critical to select the one that best matches your financial condition.

- Fees: Mortgage fees might include, among other things, origination fees, application fees, and inspection fees. While considering mortgages, keep these charges in mind.

- Down Payment: The down payment is the amount of money that you will need to put down beforehand. A larger down payment can reduce your monthly payment as well as the total amount you pay over the loan’s term.

- Prepayment penalties: If you pay off your mortgage early, some lenders may charge you a penalty. Before choosing a lender, make sure to clarify pre-payment penalties.

- Customer service: It is important to choose a lender who delivers excellent customer service and is easy to work with. To choose a lender who suits your needs, read internet reviews and ask for suggestions from friends and relatives.

What is Mortgage Escrow?

Your lender will set up a mortgage escrow account to hold funds for property taxes and insurance premiums. A portion of your mortgage payment is transferred into an escrow account each month to cover these expenditures when they become due.

What is Mortgage Amortization?

Mortgage amortization refers to the process of repaying a mortgage over time through monthly installments. Each payment is divided between repaying the principal and paying the interest on the loan. At the start of the loan term, the majority of the payment goes towards interest, but later in the loan period, more of the payment goes towards principal reduction.

How does a Down Payment Work?

A down payment is the amount of money paid ahead by a homebuyer when purchasing a property. It is often a proportion of the overall purchase price, with the mortgage loan covering the remainder of the purchase price.

The down payment required varies based on the lender and loan type, but it is normally 3% to 20% of the buying price. The more money you put down, the lower your monthly mortgage payments and the less interest you will pay over the life of the loan.

A greater down payment can also help you qualify for a lower interest rate and make you a more appealing candidate to lenders. When acquiring a home, you should carefully analyze your financial circumstances and establish what amount of down payment makes the most sense for you.

What is Private Mortgage Insurance?

Private mortgage insurance (PMI) is an insurance policy that covers the lender in the event of a loan default. PMI is typically required if the borrower puts down less than 20% of the purchase price as a down payment.

What is a Promissory Note?

A promissory note is a legal document that details the terms of a loan, such as an amount borrowed, interest rate, and repayment date.

The note provides proof of the borrower’s promise to repay the debt.

What is Mortgage Underwriting?

Mortgage underwriting is the process of evaluating a borrower’s financial information and creditworthiness in order to decide whether or not they qualify for a mortgage loan.

Repaying the Mortgage

Mortgage repayment is a crucial component of homeownership. Most mortgages have a predetermined repayment schedule, often ranging from 10 to 30 years, during which the borrower must make monthly payments to the lender in order to pay off the loan.

The monthly mortgage payment is made up of two parts: Principal & Interest. The principal is the amount borrowed, and the interest is the cost of borrowing that amount. The amount of interest paid each month is determined by the interest rate and the loan balance.

Certain mortgage payments may include escrow payments for property taxes and homeowners insurance in addition to principal and interest. The lender will normally collect these payments and hold them in an escrow account until they are due.

How to Pay off Mortgage Fast

Paying off a mortgage payment early can help you save money in the long run and achieve financial freedom sooner. Here are some tips to help you pay off your mortgage faster:

- Increase your mortgage payments: Making bigger monthly payments will help you pay off your mortgage faster and save money on interest over the term of the loan.

- Make extra payments: Making extra payments, such as an extra payment once a year or putting any excess income towards your mortgage, will also help you pay it off faster.

- Refinance to a shorter loan term: You can save money on interest by refinancing to a shorter loan term, such as a 15-year mortgage instead of a 30-year mortgage.

- Consider bi-weekly payments: Making bi-weekly mortgage payments rather than monthly installments will help you save money and pay off your home faster.

- Make lump sum payments: Making larger monthly payments will allow you to pay off your mortgage faster and save money on interest over the loan’s duration.

Remember that paying off your mortgage early might give long-term financial benefits, but it’s important to evaluate your overall financial goals and budget before making any decisions.

FAQs (Mortgage Questions)

Why do people need Mortgages?

People often use mortgages when buying a house since they do not have enough money for the total purchase price upfront. They can stretch the expense over time with a mortgage and make reasonable monthly payments.

Can anybody get a Mortgage?

Not everyone is eligible for a mortgage. When deciding whether to accept you for a mortgage, lenders will analyze factors such as your credit score, income, and debt-to-income ratio.

How much can I borrow for a Mortgage?

The amount you can borrow for a mortgage is determined by various factors, including your income, credit score, debt-to-income ratio, and the purchase price of the home.

How many Mortgages can I have on my home?

It is possible to have more than one mortgage on a home, but qualifying for a second mortgage can be challenging. Lenders often want a considerable amount of equity in the property as well as a solid credit score.

How much money do I require for a down payment?

The amount of down payment necessary for a mortgage varies based on the type of loan and the lender. To avoid private mortgage insurance, a down payment of at least 20% is generally advised (PMI).

Can I Refinance my Mortgage?

Yes of course, you can refinance your mortgage to acquire a lower interest rate, lower your monthly payment, or shorten the length of your loan.

What is a Mortgage Servicer?

The organization that manages your mortgage loan on behalf of the lender is known as a mortgage servicer. The servicer is in charge of collecting payments, keeping escrow accounts, and dealing with any issues that emerge during the loan’s term.

What is APR?

APR stands for the annual percentage rate and is the overall cost of a mortgage loan expressed as an annual percentage, including the interest rate and any other fees or penalties. The annual percentage rate (APR) is a useful metric for comparing mortgage loans from different providers.

What does “conforming” mean?

Conforming loan is a mortgage that conforms to the rules established by Fannie Mae and Freddie Mac, the government-sponsored companies that buy and sell mortgages. Conforming loans have lower interest rates and periods than non-conforming loans.

Thanks for visting, your code is: THELOVE.COM

Conclusion

In conclusion, a mortgage is a loan that you take out to buy a property, and there are various types of mortgages available in the United States, each with its own features and benefits.

When looking for a mortgage, compare rates and fees from different lenders to discover the best offer. Buying a house is a huge financial decision, and understanding the mortgage process can help you make an informed choice.