{kind=link}

I. Introduction to Mortgage Payments

A. Definition of a Mortgage A mortgage is a loan specifically used to purchase real estate. It’s typically paid back over a set period, with monthly payments that cover both principal and interest.

B. Importance of Understanding Mortgage Payments Understanding mortgage payments is crucial for homeowners as it determines their financial obligations over the loan term. Accurately calculating payments ensures budgeting and financial stability.

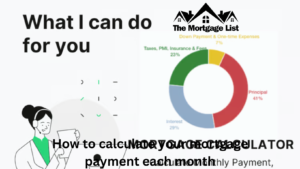

C. Overview of Mortgage Payment Calculation Mortgage payments consist of principal, interest, taxes, and insurance. The calculation varies based on loan type, interest rate, loan amount, and other factors.

II. Components of Mortgage Payments

A. Principal The principal is the initial amount borrowed to purchase the property.

B. Interest Interest is the cost of borrowing money from the lender, calculated as a percentage of the principal.

C. Taxes Property taxes are levied by local governments based on the property’s assessed value.

D. Insurance Homeowner’s insurance protects against property damage and liabilities.

E. Private Mortgage Insurance (PMI) PMI is required for conventional loans with a down payment less than 20% of the home’s value.

III. Understanding Mortgage Payment Formulas

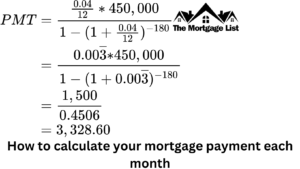

A. Calculation of Fixed-Rate Mortgage Payment Over the course of the loan term, fixed-rate mortgages feature equal monthly payments and fixed interest rates. The amortizing loan formula can be used to determine the monthly payment.

B. Adjustable-Rate Mortgage (ARM) Payment Calculation ARMs have variable interest rates that fluctuate with market conditions. Initial payments are typically lower but can increase over time. Calculating payments involves using the initial rate and adjusting it based on future rate changes.

C. Amortization Schedule An amortization schedule details each mortgage payment, breaking down how much goes towards principal, interest, taxes, and insurance.

D. Using Mortgage Payment Calculators Online calculators simplify the process by automatically computing monthly payments based on inputted data.

IV. Step-by-Step Guide to Calculate Mortgage Payments

A. Gather Necessary Information Collect information such as loan amount, interest rate, loan term, property taxes, insurance premiums, and PMI rates.

B. Calculate Principal and Interest Use the appropriate formula to determine the monthly principal and interest payments.

C. Estimate Property Taxes and Insurance Estimate annual property taxes and insurance premiums, then divide by 12 to determine monthly amounts.

D. Include PMI if Applicable If the down payment is less than 20%, factor in PMI payments.

E. Determine Total Monthly Mortgage Payment Add up principal, interest, taxes, insurance, and PMI (if applicable) to calculate the total monthly mortgage payment.

V. Factors Affecting Mortgage Payments

A. Loan Amount Higher loan amounts result in higher monthly payments.

B. Interest Rate Lower interest rates reduce monthly payments and overall loan costs.

C. Loan Term Shorter loan terms result in higher monthly payments but lower overall interest costs.

D. Down Payment A larger down payment reduces the loan amount, resulting in lower monthly payments.

E. Credit Score Borrowers with higher credit scores qualify for lower interest rates, reducing monthly payments.

VI. Strategies for Managing Mortgage Payments

A. Refinancing Refinancing to lower interest rates or adjusting loan terms can reduce monthly payments.

B. Making Extra Payments Making additional principal payments reduces the loan balance and shortens the loan term.

C. Biweekly Payment Plans Biweekly payments result in one extra payment per year, accelerating loan payoff.

D. Considering Government Programs Government programs offer assistance to homeowners struggling with mortgage payments.

VII. Common Mistakes to Avoid

A. Underestimating Total Costs Failure to consider all costs can lead to budget shortfalls.

B. Ignoring Interest Rate Fluctuations Ignoring rate changes can result in unexpected payment increases.

C. Not Factoring in PMI Not including PMI in calculations can lead to inaccurate estimates.

D. Neglecting Escrow Account Changes Changes in taxes or insurance premiums can affect monthly payments.

VIII. Conclusion

In conclusion, mastering the calculation of mortgage payments is an essential skill for homeowners, enabling them to navigate the complexities of homeownership and maintain financial stability. By understanding the components of mortgage payments, including principal, interest, taxes, insurance, and potential PMI, individuals can accurately assess their financial commitments and budget effectively.

Moreover, familiarity with various mortgage payment formulas, such as those for fixed-rate mortgages, adjustable-rate mortgages (ARMs), and amortization schedules, equips homeowners with the tools needed to calculate monthly payments accurately.

Factors influencing mortgage payments, such as loan amount, interest rate, loan term, down payment, and credit score, highlight the importance of thorough financial planning and strategic decision-making.

Furthermore, implementing strategies like refinancing, making extra payments, enrolling in biweekly payment plans, and exploring government assistance programs can help homeowners manage their mortgage payments more effectively and potentially save on overall costs.

Avoiding common mistakes, such as underestimating total costs, ignoring interest rate fluctuations, neglecting PMI, and overlooking changes in escrow accounts, is critical for maintaining financial health and avoiding budgetary surprises.

In essence, by following the comprehensive guide outlined above and taking proactive steps to manage mortgage payments, homeowners can navigate the homeownership journey with confidence, ensuring long-term financial security and peace of mind.

Read More:>