{kind=link}

Introduction Short Refinance

In the realm of mortgage finance, the term “short refinance” may not be as familiar as traditional refinancing options. However, for homeowners facing financial challenges or seeking better terms on their existing mortgage, short refinance presents a compelling solution. This comprehensive guide aims to demystify the concept of short refinance, exploring its benefits, eligibility criteria, application process, and frequently asked questions.

Definition and Importance

Short refinance, also known as mortgage restructuring or loan modification, involves renegotiating the terms of an existing mortgage to alleviate financial strain or secure more favorable terms. Unlike traditional refinancing, which replaces the original loan with a new one, short refinance aims to restructure the existing loan to make it more manageable for the borrower. This option is particularly beneficial for homeowners facing financial hardship or those with underwater mortgages.

Understanding Short Refinance

Differentiating from Traditional Refinancing

Short refinance differs from traditional refinancing in its approach and objectives. While traditional refinancing involves obtaining a new loan to replace the existing one, short refinance focuses on modifying the terms of the current mortgage to improve affordability or address financial challenges. This distinction makes short refinance an attractive option for borrowers who may not qualify for conventional refinancing due to credit issues or insufficient equity.

Benefits of Short Refinance

Alleviating Financial Strain

One of the primary benefits of short refinance is its ability to alleviate financial strain for homeowners facing difficulty in meeting their mortgage obligations. By renegotiating the terms of the loan, such as lowering the interest rate, extending the repayment period, or reducing the principal balance, short refinance can make monthly payments more affordable and sustainable for the borrower.

Avoiding Foreclosure

Short refinance also serves as a valuable tool for homeowners at risk of foreclosure. By restructuring the mortgage to improve affordability, borrowers can avoid the devastating consequences of foreclosure and retain ownership of their homes. Lenders may be willing to negotiate terms through short refinance to mitigate losses associated with foreclosure proceedings.

Eligibility Criteria

Financial Hardship

To qualify for short refinance, borrowers typically need to demonstrate financial hardship, such as job loss, medical expenses, divorce, or other circumstances affecting their ability to pay the mortgage. Lenders may require documentation to substantiate the hardship claim and assess the borrower’s eligibility for loan modification.

Loan-to-Value Ratio

Another crucial factor in short refinance eligibility is the loan-to-value (LTV) ratio, which compares the outstanding loan balance to the current market value of the property. Borrowers with significant negative equity, where the loan balance exceeds the property’s value, may be prime candidates for short refinance. However, lenders may impose limits on LTV ratios to mitigate risk.

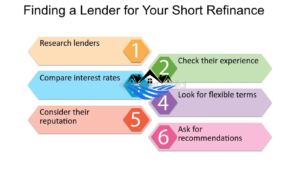

Application Process

Contacting the Lender

The first step in pursuing short refinance is to contact the lender or loan servicer to express the intent to explore loan modification options. Borrowers should be prepared to provide detailed information about their financial situation, including income, expenses, assets, and liabilities.

Submission of Documentation

Upon initiating the short refinance process, borrowers will be required to submit documentation to support their request for loan modification. This may include pay stubs, tax returns, bank statements, hardship letters, and any other relevant financial records. The lender will review the documentation to assess the borrower’s eligibility and determine the appropriate course of action.

Interest Rates and Terms

Negotiating New Terms

During the short refinance process, borrowers have the opportunity to negotiate new terms for their mortgage, including interest rates, loan duration, and repayment terms. The goal is to secure more favorable terms that align with the borrower’s financial capabilities and long-term goals. Lenders may be willing to adjust the terms to prevent default and minimize losses.

Impact on Credit Score

It’s important to note that short refinance may have implications for the borrower’s credit score. While loan modification itself may not directly impact credit scores, any missed payments or delinquencies leading up to the refinance process could negatively affect creditworthiness. Borrowers should weigh the potential impact on their credit score against the benefits of short refinance before proceeding.

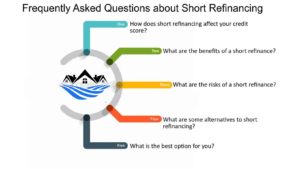

Frequently Asked Questions

- What Is Short Refinance? Short refinance, also known as mortgage restructuring or loan modification, involves renegotiating the terms of an existing mortgage to alleviate financial strain or secure more favorable terms.

- Who Qualifies for Short Refinance? To qualify for short refinance, borrowers typically need to demonstrate financial hardship and have a loan-to-value ratio that meets the lender’s criteria. Documentation of hardship and financial standing may be required.

- What Are the Benefits of Short Refinance? Short refinance offers benefits such as reduced monthly payments, avoidance of foreclosure, and improved long-term affordability for homeowners facing financial challenges or underwater mortgages.

- How Does Short Refinance Differ from Traditional Refinancing? Short refinance differs from traditional refinancing in its approach and objectives. While traditional refinancing involves obtaining a new loan to replace the existing one, short refinance focuses on modifying the terms of the current mortgage to improve affordability or address financial challenges.

- What Is the Impact of Short Refinance on Credit Score? Short refinance may have implications for the borrower’s credit score, particularly if there are missed payments or delinquencies leading up to the refinance process. Borrowers should consider the potential impact on creditworthiness before pursuing short refinance.

- Can Short Refinance Help Avoid Foreclosure? Yes, short refinance can help homeowners avoid foreclosure by renegotiating the terms of the mortgage to make it more affordable and sustainable. Lenders may be willing to work with borrowers facing financial hardship to prevent foreclosure and minimize losses.

Conclusion

In conclusion, short refinance offers a viable solution for homeowners facing financial challenges or seeking better terms on their mortgages. By renegotiating the terms of the existing loan, borrowers can alleviate financial strain, avoid foreclosure, and secure more favorable terms tailored to their needs. However, eligibility criteria, application process, and potential credit implications should be carefully considered before pursuing short refinance. With proper understanding and guidance, short refinance can be a valuable tool in achieving long-term financial stability and homeownership success.

Read More:>